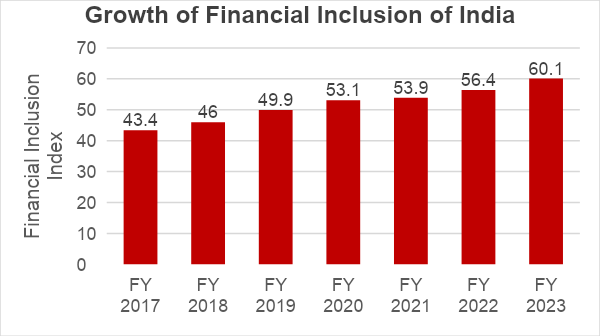

Fintechs and Bigtechs have driven advances in financial inclusion, particularly in Asia. While Govt. pushes for more financial inclusion, the use of personal data by Bigtechs and other companies raises important questions about consumer protection & privacy. In the recent years, the steady growth of financial inclusion in India is a hallowed story. As per McKinsey survey in Aug 2023, Indian banks have around 78% penetration of bank accounts. The pandemic increased the pace of digital transaction, with more than 80mn public making their first digital merchant transaction after the start of the pandemic. As of the fiscal year 2023, the financial inclusion index of India was 60.1, according to the Reserve Bank of India. It rose from 43.4 in 2017 to its current state, indicating improved financial inclusion. The financial inclusion index measures the extent of access to and usage of formal financial services, including banking, insurance, investments, pensions, and postal sectors.

Graph1: Growth of Financial Inclusion Index of India over years

Source: Statista 2024

Fintech evolution got a boost from Govt’s digital public infrastructure

India’s financial landscape has gone through a monumental transformation in recent years. The implementation of the country’s digital public infrastructure, which includes Adhaar (digital ID system), Unified Payments Interface (fast payments system) and DigiLocker (digital document wallet) has not only revolutionised the payment system but also changed the financial inclusion landscape in India. Without Digital Payment Infrastructure (DPI) such as Jan Dhan Bank accounts, Aadhaar, and Mobile phones (the JAM trinity), India may have taken 47 years to achieve financial inclusion rate of 80% which the country has achieved in just six years, says a G20 policy document prepared by the World Bank. “In just six years, it (the India stack) has achieved a remarkable 80% financial inclusion rate — a feat that would have taken nearly five decades without a DPI approach. Implementation of DPIs such as Aadhaar, along with the Jan Dhan bank accounts and mobile phones, is considered to have played a critical role in moving ownership of transaction accounts from approximately one-fourth of adults in 2008 to over 80 percent now,” the report says. The interoperability allows private companies to integrate apps with state services, providing consumers with access to various services, including social benefit transfers, bill payments and loan applications. With more than 300 million users, the current UPI ecosystem is capable of handling up to 100bn transactions monthly.

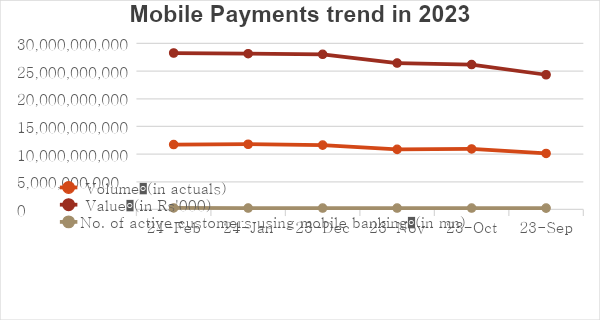

As per Reserve Bank of India, more than 260mn mobile banking account holders have conducted more than 11.7bn transactions with value more than 28.2 tn rupees in the month of Feb 2024 alone.

As we see the data released by the Reserve Bank of India (i.e. Central Bank of India) in the graph below (Graph 2), there is a steady growth of active users with growing volume and value of transactions, which are largely from the retail consumer segment. Similarly, we see a significant jump in app based mobile payments in the last one year (Graph 3).

Graph 2: Mobile Payments trend in 2023

Graph 3: Growth of App based Mobile Payments in the last 6 months

The ecosystem of DPI, telecom and fintech organizations pioneering financial Inclusion

As research says, in developing countries, financial inclusion is constrained by the cost of transactions and various systemic risks. However, in India, fintech organizations capitalised on the Digital Payment Infrastructure system build by Govt. that removed the transaction costs of small value transactions, penetrating the vast rural unbanked segment. The prior telecom revolution and central bank’s opening of banking licenses with specialised banks such as payment banks and small finance banks fostered the growth deep into rural India.

Proportion of men and women at each stage of the mobile money user journey

in 2023 by country (percentage of the total adult population)

Graph 4: Use of Mobile Money

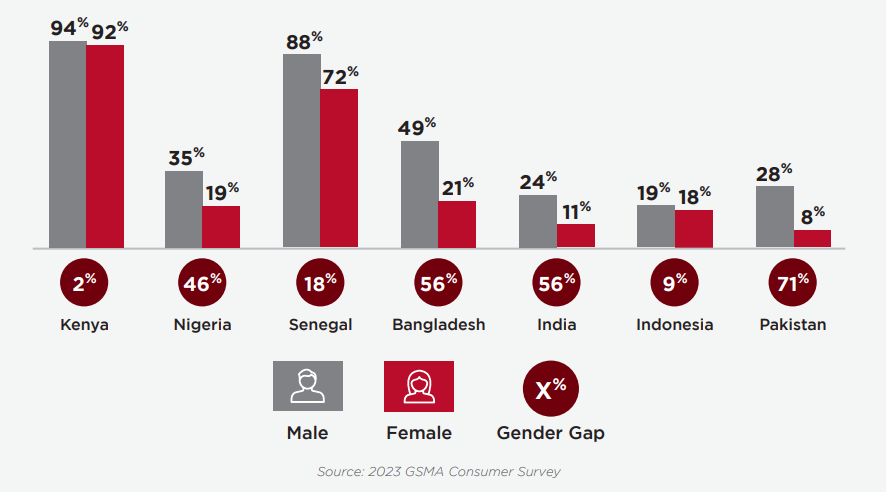

As the graph below (Graph 5) shows, there exists a significant gender gap in mobile money account ownership in India as per the GSMA survey 2023. This calls for more female empowerment and engagement in financial matters.

Mobile money account ownership in 2023 (% of the total adult population)

Graph 5: Mobile money account ownership in 2023

Key concerns aiding the Systemic Risks:

- Moving money at a click of a button in mobile may sometimes lead to unintended and unknown consequences. This level of technological advancement is far beyond the comprehension of the targeted public under financial inclusion programs.

- The blurred boundaries between fintech plays and banking regulators creates more systemic issues, as they obfuscate the strict regulatory controls applicable to banks. To retain public trust and safety, regulators need to move swiftly while inter-connection between technology and markets increases.

Challenges:

- Bridging the gap to the next 250 to 300m users requires concerted efforts in enhancing financial literacy and expanding proliferation of smartphones in the country.

- Development in AI enabled cyber crimes- Hackers and state sponsored actors may out grow the security systems faster generating more innovative ways defraud public. With lower digital literacy and awareness, more innocent public may fall prey.

- Cash is still the king in rural segments.

- Lack of knowledge leading to trust deficiency.

Salient points covered:

On a broader note, we have discussed the following points in the article:

- Financial inclusion is fueled by financial innovation by extending banking facilities to unbanked segments.

- Fintechs and Bigtechs have triggered financial inclusion in developing countries especially in India. However, since it deals with sensitive consumer information, data privacy needs to be protected.

- Though India has achieved substantial growth in financial inclusion in recent years, there is still plenty of room for further growth in future.

- DPI played a major role in eliminating entry barriers and proved to be a critical success factor in this growth.

- Private players need to collaborate with Govt. agencies to augment this journey making it more successful and comprehensive in future.

Call to action:

- Govt. should create programs partnering with banks & financial institutions, fintechs and telecom players boost financial and digital literacy by allocating budget.

- Banks and financial institutions should work together with Fintechs to innovate new offerings at lower transaction cost. This will also help Fintechs enabling further penetration into remote rural areas providing the last mile of coverage.

- Govt. can work with Fintechs and Regtechs on how digital technologies like AI can be deployed for data protection and proactively detect and prevent cyber attacks.

Authors:

Sachio Nishioka

Senior Partner, DXC Technologies, Singapore

(https://www.linkedin.com/in/sachio-nishioka-3b067420/)

Bhushan Joshi

Competency Leader, IBM, India

(https://www.linkedin.com/in/joshibhushan/)

Manas Ranjan Panda, PhD

Partner, Wipro Limited, USA

(https://www.linkedin.com/in/manaspanda01/)

Raja Basu

Financial Markets Leader and SME, IBM, India