Embedded insurance, an extension of the embedded finance ecosystem, is a marriage of insurance functionality into technology; it enables businesses to weave insurance into their infrastructure, customer experiences, and products through third-party platforms and application programming interfaces (APIs).

Embedded insurance can be offered as:

- a complimentary add-on to the core offering of the business

(a bundling of insurance with the sale of a car); - at point of sale

(marketplaces offering insurance cover for expensive goods); - as a part of invisible native components

(complementary insurance cover as part of Uber’s contract with its drivers).

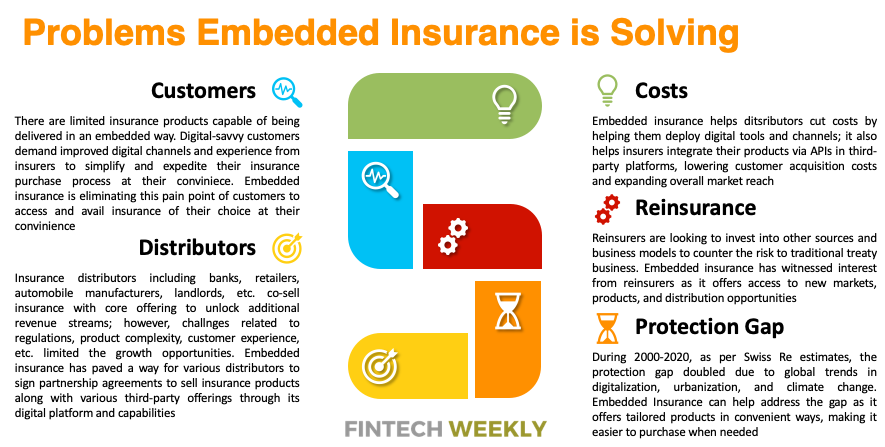

In a wake of rapid digitalization where consumers are increasingly buying products online, businesses across industries require an online presence to remain competitive. Further, the evolving consumer preferences are favouring the change of buying products online - presenting an opportunity for companies to reap the benefits of consumer lifestyle changes by integrating various financial services including insurance most conveniently and seamlessly within online customer journeys.

Embedded insurance is reshaping the insurance market with a necessary digital touch which should be embraced as an opportunity instead of a threat. Companies such as Railsbank and Certua have provided modern-age technical capabilities to help businesses integrate insurance, payments, and other financial services.

Embedding insurance expands accessibility for all insurance types by introducing coverage at the moment it is needed and at the point where the consumer is most likely to buy. For instance, the consumer is offered the choice to avail of insurance to cover future medical bills, including vaccines and wellness during a visit to the veterinarian for a pet. A similar scenario is also taking place in the travel industry where providers, such as airlines, hotel chains, and theme parks are providing consumers with the option to safeguard their trip with travel insurance availed as a part of the initial reservation booking.

A New Wave in the Insurance Industry

As per Bain & Company predictions, broad-scale market penetration is likely to begin across the three lines of coverage including auto, travel and property.

Instech London estimates that the global embedded insurance will grow to $722 billion by 2030, nearly six times of 2022 value. The US market is expected to reach a value of $70.7 billion in 2025 from $5 billion in 2020. McKinsey estimates that up to 25% of personal line premiums and 30% of auto premiums can be generated through embedded ecosystems by 2030.

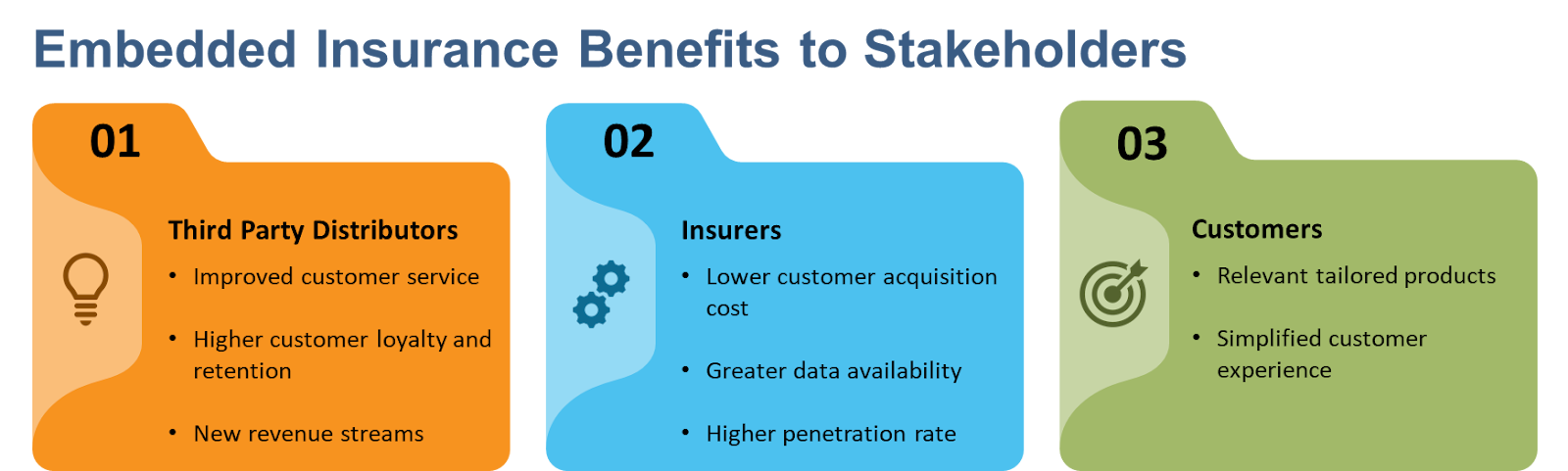

Embedded insurance enables businesses to bring down distribution costs through the integration of various insurance products in third-party ecosystems. Embedded insurance can benefit all the stakeholders involved including third-party distributors, insurers, and customers.

Embedded insurance’s involvement with third-party platforms redefines the role of insurers, a fundamental shift in how the insurance industry operates. The change would require insurers to innovate and strengthen technology infrastructure to maintain their competitiveness and protect profitability.

Types of Embedded Insurance

-

Related Embedding: Offers end-user insurance digitally within the partner's ecosystem. It is not dependent on a transaction between the non-insurance partner and the end client. For example, a car dealer's blog about how to choose a car leads a buyer to an insurance-related page with an advertisement.

-

Linked Embedding: Also known as Soft Embedding where partners’ point of sale is converted into an insurance sales channel. Typically, contextually applicable insurance coverage is offered alongside the non-insurance product, with relevant features, pricing, and exclusions without any information. Purchasing such insurance is voluntary for the end user, but its urgency can help convert the decision.

-

Bundle Embedding: Also referred to as Hard Embedding where the cost of the non-insurance product consists of the coverage but is mostly advertised as a freebie. The end user does not have the option to refuse coverage. Under this option, the end user is shared between an insurance company and a non-insurance service provider.

What’s the Right Approach?

The embedded insurance has a huge potential considering the combined downstream and upstream opportunities. Partnerships with third-party companies will play a crucial role as insurance distribution expands outside the traditional bounds. On the technical front, the major obstacles still need to be overcome. The majority of insurers face challenges with the limitations and reliance on legacy systems, which makes it difficult for them to seamlessly plug into new digital ecosystems. The capacity to build and quickly configure appealing customer journeys with capabilities to sample innovative offerings and business models are prerequisites for effective involvement in the evolving embedded insurance ecosystem.

Insurers will need to evaluate their strengths and innovation requirements to plug any gaps to capitalise on the embedded opportunity, which will eventually help them cement their place in the market. Insurers with significant Omni channel capabilities, smooth claim disbursements, and constant touch with customers are likely to have the upper edge in this intensifying embedded insurance market.